Introduction

Quick! What’s the first thing that comes to your mind when you hear the word retirement? A rocking chair? Endless beach strolls? Daily trips to the range?

The traditional retirement model was built for a different era, when lifespans were shorter and retirement lasted years, not decades. Today, something different is emerging. A recent study found that 84% of workers plan to work in some capacity in retirement, up from 75% three years before. We call this shift “Life After Work” — a realistic perspective and acknowledgment that work, in some form, doesn’t have to end.

Naturally, redefining retirement affects everything from your financial strategy to your future endeavors and sense of purpose. Embracing it requires a new mindset.

Retirement No Longer Means A Hard Stop

For decades, retirement was a clean break from work. One day you’re making key decisions in the boardroom; the next, you’re adjusting your golf swing. This all-or-nothing approach can lead to financial and psychological whiplash, not to mention a loss of purpose. No wonder that, for many, retirement is followed by depression and sometimes even cognitive decline.

| New thinking: The rigid retirement model is losing its grip on society. Today, high-achieving professionals and business owners are looking for a gradual shift that leverages their expertise, maintains their sense of identity, and provides financial flexibility. Approached this way, your transition is in your hands, allowing you to decide how much you work and for how long. |

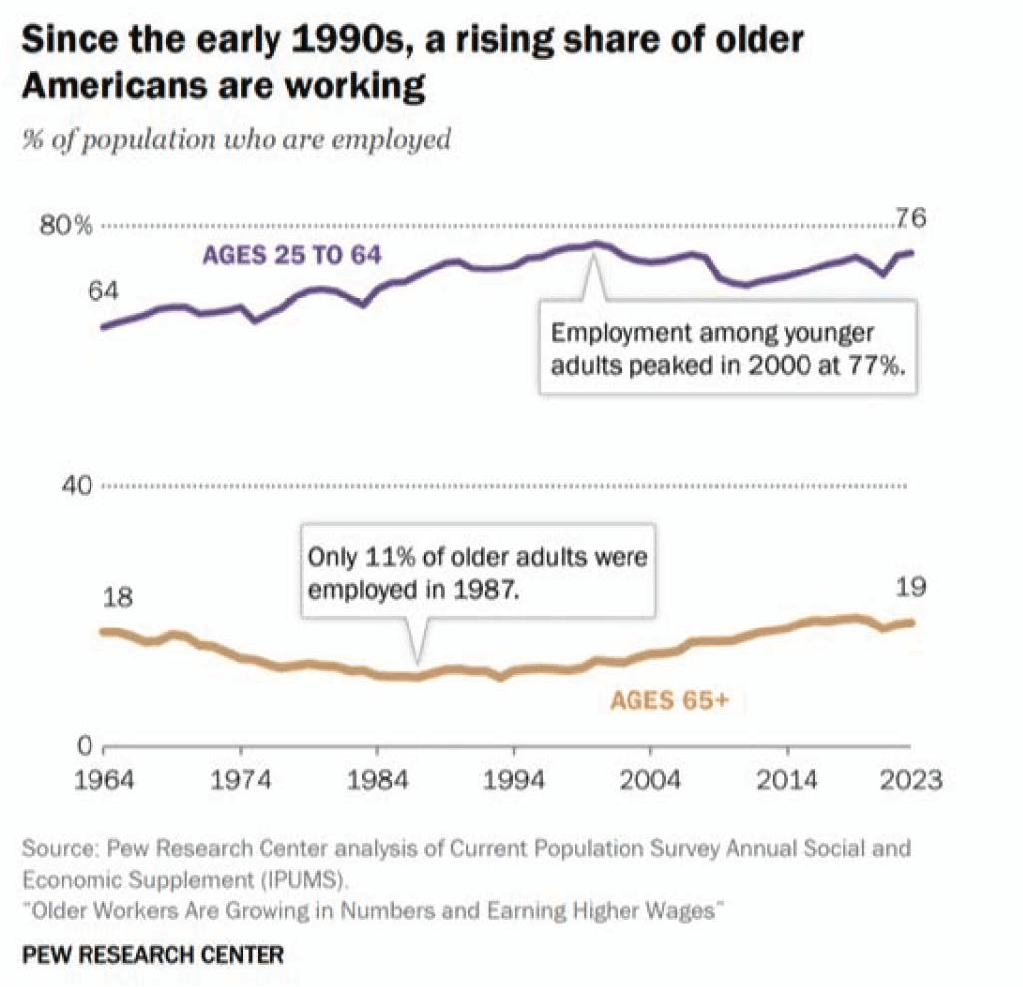

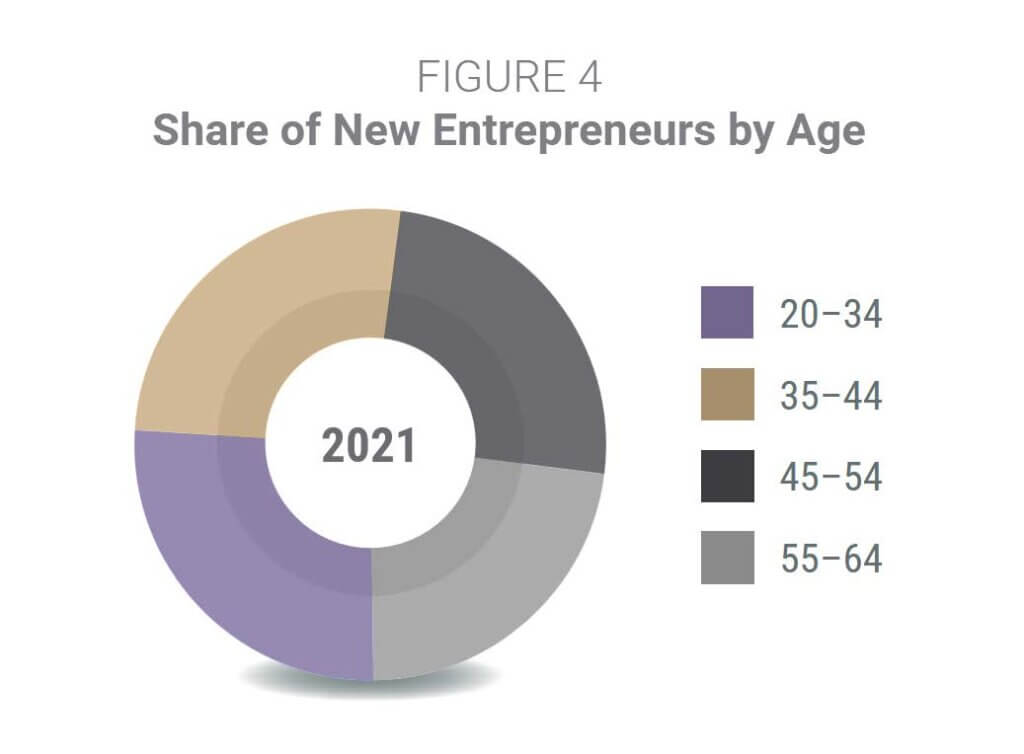

Life After Work gives you the best of both worlds: more time for leisurely pursuits while staying engaged and potentially generating income. This is no longer a fringe concept. Research from the Pew Research Center shows that workforce participation among those 65 and older has been steadily rising since the 1990s. Consider former NFL quarterback Tom Brady, who announced his retirement from football after 22 seasons only to have a change of heart 40 days later. Brady’s brief stint away from football highlights how even elite professionals struggle with the abrupt transition from a career that defined their identity to the next phase of life. When he eventually retired for good, Brady had lined up broadcast opportunities and business ventures, demonstrating (quite aptly) the modern approach of evolving careers rather than stopping work entirely. Work at this stage can take many forms. It can be a matter of reducing your hours with your employer, taking on a consulting role, or even launching a business. In fact, 22.8% of new businesses are launched by people aged 55 to 64, an 8% increase from 1996.

A Stable Retirement Rests On Flexible, Not Fixed Income

Conventional retirement centers around predictable, fixed-income streams like Social Security, pension payments, and regular withdrawals from your retirement accounts. In this scenario, retirees wind down their spending during their “golden years,” and they need less (but still predictable) income.

| New thinking: Life After Work often involves a different set of financial considerations. By making consulting, a new business, project-based work, or passive income a part of your retirement planning, you no longer have to rely solely on your nest egg for income. |

Flexibility is integral to a modern post-career life. Many retirees today are healthier and more active than previous generations, leading to higher spending in the early years of retirement. And with higher inflation recently, more retirees are returning to the workforce to make their assets last longer. That said, sustaining your earnings doesn’t necessarily translate to more simplicity — variable income sources require more sophisticated financial strategies beyond standard withdrawal rules.

Arbitrary Age Milestones No Longer Fit Modern Lives

Our retirement system is built around rigid age thresholds: Social Security at 62 to 70, Medicare at 65, required minimum distributions (RMDs) starting at 73. However, they incorrectly assume that everyone follows the same chronological career path. If you continue earning income past what we conventionally think of as “retirement age,” these milestones become increasingly arbitrary and outdated.

| New thinking: High-achievers are rewriting the rules of work. Many hit their professional stride in their 50s and 60s, some even starting new ventures. Life After Work isn’t tethered to a specific age — it revolves around your own desired timeline. |

Working longer can bolster your finances. It helps you delay claiming Social Security and increase your monthly benefit. While you are earning income, you may be able to delay taking your RMDs, allowing your retirement accounts to grow in a tax-advantaged way.

On the other hand, it also introduces complexities because our retirement system is, of course, tied to traditional milestones.

- Medicare enrollment: While you can delay Social Security benefits, Medicare has strict enrollment windows. If you’re still covered by employer health insurance at 65, you must apply for a Special Enrollment Period in order to avoid late enrollment penalties that could increase premiums for the rest of your life.

- Social Security earnings test: If you claim Social Security early while still working, you may trigger the earnings test, in which a portion of your Social Security will be taxable. In 2025, if you are younger than full retirement age (currently 66 to 67 years old) and earn more than $23,400, you will lose $1 in benefits for every $2 you earn above this threshold, amounting to a 50% reduction on your earnings.

- RMDs: Regardless of whether you’re still working past age 73, you must take RMDs from your previous employers’ retirement plans and individual retirement accounts — even if you don’t need the money. These forced withdrawals could create unwanted taxable income.

- Investment strategy: Traditional asset allocation models such as those used by target-date funds assume retirement at conventional ages. But that might be too conservative for your actual timelines and goals, potentially limiting your portfolio’s growth opportunity. By earning income outside your retirement account, you may have a buffer to take additional risk — and potentially generate higher returns.

Saving Too Much By Missing Out On Life Today

Retirement planning can often encourage over-saving at the expense of living fully today. It’s understandable how this became go-to retirement saving advice, given that large swaths of workers don’t have enough retirement savings. But in the process, it’s created a “work, save, die” paradigm that few find satisfying.

| New thinking: Life After Work strikes a balance. By maintaining some income through meaningful work, you can reduce the pressure on your investment portfolio, giving you some breathing room. What’s more, additional income streams could extend the lifespan of your portfolio by years. |

In addition, you may also be able to:

- Reduce the need for unwanted frugality in the pre-retirement years

- Keep your mind sharp through continued engagement

- Create financial flexibility to handle market downturns and offset portfolio losses

- Fund “bucket list” experiences without guilt or financial strain

The Life After Work approach encourages a holistic view of wealth that includes experiences, relationships, health, and purpose. In other words, all the things that go into making your life meaningful.

The Most Important Factor In Retirement Readiness May Not Be Financial

Traditional retirement planning focuses almost exclusively on financial readiness. Leaving your job typically comes down to a simple calculation: when can your nest egg generate enough income to replace a certain percentage of your salary? What this approach fails to address is whether you’re emotionally prepared for the next phase.

| New thinking: When your answer to “What do you do?” changes from “I’m the CFO at Company X” to “I’m retired,” there’s an inevitable identity shift. |

For high-achievers, work is more than income. It’s how many derive their purpose, structure their days, and create social connections. Without adequate preparation for this professional passage, even the most financially well-off retiree can struggle without direction. That’s why in the years leading up to your exit, it’s important to think about not just what you’re retiring from, but what you’re retiring to. The most successful retirees have a road map for what their purpose will be once they leave the daily grind behind. Their top goal isn’t “relaxing” or “taking it easy.” Instead, they embrace Life After Work as a time to learn new things, be of service, or find meaning in new ways.

Life After Work planning should outline ways to maintain social connections and intellectual stimulation. These non-financial aspects of retirement planning are often the difference between merely existing in retirement and truly thriving in this new environment.

Creating Your Life After Work Strategy

True financial freedom is achieved through autonomy to work on your terms. Life After Work gives you control over your time, energy, and expertise — but it requires planning.

Purpose Planning

Understand what type of work you want to do during Life After Work by identifying transferable skills for your next chapter. You might need to upskill your professional knowledge to fill any gaps or hone skills to stay competitive.

Transition Timeline Design

Develop a flexible road map for scaling back traditional work while you build a runway for new ventures. Start planning 18 to 24 months in advance.

Financial Modeling for Variable Income Streams

Fluctuating income needs more planning than a regular paycheck. Create tax efficient withdrawal strategies that adapt to changing income. Balance investments for growth and stability during your transition years.

Take The First Step Toward Redefining Your Future

Leaving your job and phasing into the next stage of life is not an easy decision. If you have concerns or lingering doubts, you’d hardly be the first person to question if now is the right time. Our goal is simple: To help you step into this next phase with the utmost confidence. A conversation is the best way to start. No pressure, no obligations — just clarity on where you stand and where you could go from here.

Schedule a free consultation with Burton Enright Welch, and we’ll start mapping out your Life After Work, together.

Sources:

1 Mercer, “Reimagining work and retirement”

2 National Institutes of Health, “Risk of Cognitive Declines With Retirement: Who Declines and Why?”

3 Pew Research Center, “The growth of the older workforce”

4 Ewing Marion Kauffman Foundation, “Trends in Entrepreneurship Series”

5 J.P.Morgan Asset Management, “Three new spending surprises: Additional insights into retirement

spending behaviors”

6 ResumeTemplates.com, “ResumeTemplates.com Survey Finds 1 in 4 Retired-Aged Seniors Are Still

Working, With More Planning to Rejoin Workforce in 2025”

7 Medicare.gov, “Working past 65”

8 Social Security Administration, “Exempt Amounts Under The Earnings Test”

9 Vanguard, “The Vanguard Retirement Outlook: A national perspective on retirement readiness”

Get the BEW Newsletter Direct to Your Inbox

Stay informed with timely perspectives and market insights from the BEW Invest team.