I. 2018 Review

In 2017, investing seemed easy. Most asset classes posted gains, volatility was nonexistent, and investors enjoyed following their portfolio balances.

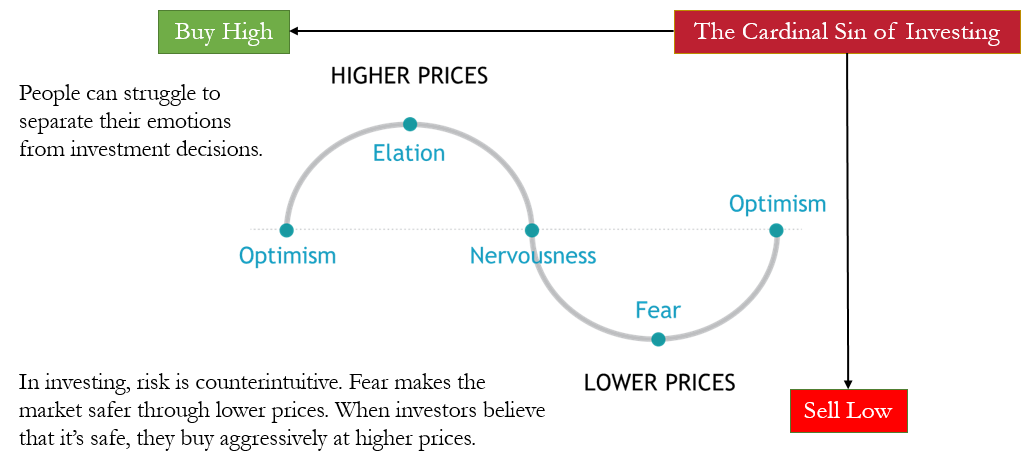

Last year reminded everyone that investing is hard. It can be uncomfortable and unpleasant. Market volatility can diminish willpower and cause determination to waver. The main risk is not portfolio declines. The real risk is that instincts override the discipline investors need to achieve their long-term plan.

Among our most important responsibilities to our clients is to fortify discipline during challenging times. Our primary tools to do so are information, experience, and structure.

2017 vs. 2018: Dr. Jekyll & Mr. Hyde

Simply put, it was extremely difficult to make money in the financial markets in 2018. Oddly, investors had the exact opposite experience in 2017.

While there is no lone reason why this happened, economist Hyman Minsky may help explain. He showed that periods of market stability can lay the foundation for dramatic instability.

Here, the persistent calm of 2017 gave investors the impression of safety and easy gains. When the news turned sour, that comfort gave way to a harsh shift in sentiment. The world did not look much different than months earlier, but investor perceptions changed markedly. In a sense, 2018’s broad weakness may have resulted from 2017’s broad strength.

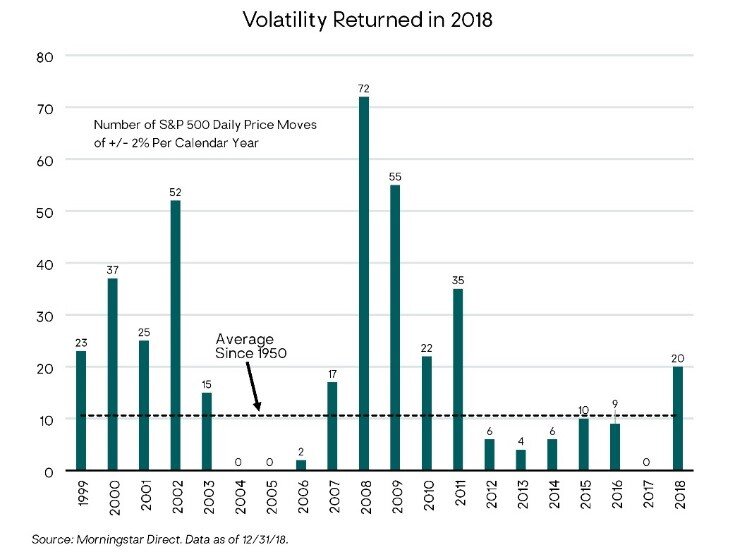

When markets headed south, especially in December, investors overreacted. There were zero days in 2017 where the S&P 500 moved more than 2% in either direction. In December 2018, there were six.

The primary characteristic shared by 2017 and 2018 was uniformity. A November Deutsche Bank study (chart below) noted that 90% of the 70 asset classes it tracks showed negative year-to-date returns. This was the highest percentage of losers in the study’s 100-year history. The lowest percentage of losers was in 2017.

In 2017, markets seemed to overlook looming challenges – trade concerns, meteoric growth in tech stocks, excessive reaching for yield in credit markets. In late 2018, asset prices started to reflect those challenges.

Thus, in at least a few ways, 2018’s downturn was productive: it reminded people that there is risk in investing, that 2017 was unsustainable, and that the baseline approach to markets should always come from a place of humility.

Asset Class Whiplash

Similar to the whiplash in the Deutsch Bank data, individual asset classes experienced a jarring 2017 to 2018 reversal.

Each of the three broad equity asset classes – U.S., Developed International (Int’l), and Emerging Markets (EM) – gave back a chunk of their 2017 returns. Their relative rankings also flipped. EM was first among equity asset classes in 2017 and last in 2018. The U.S. was the opposite: last in 2017 and first in 2018.

The S&P 500 had its first negative year since 2008. Through September, the S&P was up 11% and looked likely to reach a record tenth consecutive calendar year of positive returns. Instead, the S&P fell 20% from Sept 20 through Christmas. It was the worst December in the S&P’s 91-year history.

An interesting side note is that international stocks, particularly emerging markets, held up better than U.S. stocks during the Q4 turmoil. U.S. stocks fell 14.3% in Q4 while emerging market stocks fell 7.4%. Whether this is a blip or a turning point remains to be seen.

While bonds provided desired stability, unusually, they did not deliver gains with stocks down. The Barclay’s Bond Index ended the year barely positive. Had it not picked up a small gain on December 31, it would have been the first time in the index’s 43-year history that bonds were down in the same year as the S&P 500.

Cash bettered stocks and bonds for the first time since 1994. With rising rates, cash savers are earning meaningful yield for the first time since the Great Recession. But don’t let higher yields excite you. Holding cash is useful in the short-term but counterproductive long-term. Cash has outgained stocks and bonds in less than 10% of 3, 5, and 10 year periods and in no 20 year periods.

The dramatic asset class reversal belies the big picture reality. The combined 2017 and 2018 results are roughly in line with our long-term expected returns.

We’ve all agreed to use the January-December calendar to mark our 365-day trip around the sun. That annual journey has nothing to do with the financial markets, and yet it crystalizes market narratives.

Our takeaway from the past two years is not that 2017 was great and 2018 was not. The broader lesson is that the market is normal when it is acting abnormally. The short-term journey may be unpredictable, but longer-term trends (especially those of five-plus years) tend to hew to a pattern.

The manner that investors earned their 2017-18 returns may have been odd. That should not obscure recognition of the progress made toward your long-term goals. Over time, fundamentals and long-term investment tenets prevail.

Where Do We Go from Here?

Our 2019 outlook is much the same as our outlook at the top of any year. The markets will likely go up. That is not based on a reading of today’s conditions, but on market history. The market is similarly likely to go up in any given year no matter the circumstances.

With this in mind, one of our largest value-adds is keeping our clients invested. Humans are hard-wired to seek safety in response to bad news and uncertainty. It is challenging for investors, us included, to not react.

Yet, the costliest mistake many people make is bailing out at the wrong time. Selling in a down market locks in losses and can risk missing a rebound. As your adviser, our role is to help you embrace (or at least be somewhat comfortable with) the short-term volatility and uncertainty. Doing so means taking appropriate risks in pursuit of attaining your long-term goals.

If there is anything in your financial picture that requires near-term certainty e.g. a cash need or a life change that we should be aware of, please let us know. We can discuss and plan for your specific situation in greater detail.

Finally, periods like 2018 illustrate why we build financial plans and Investment Policy Statements (IPS). They provide the structure and long-term perspective that can be necessary reminders during downturns. Please let us know if you would like to revisit your financial plan or IPS with us.

Get the BEW Newsletter Direct to Your Inbox

Stay informed with timely perspectives and market insights from the BEW Invest team.