I. A Surprising First Half

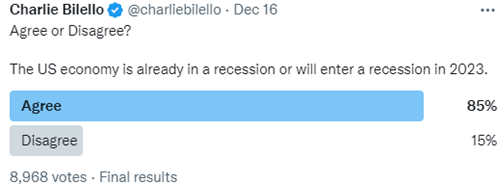

Entering 2023, chatter fixated on the inevitable and impending recession. How deep would it be? How would the Fed respond? Would this solve inflation?

Six months later, recession talk is still common. Meanwhile, stocks have rallied. The S&P 500 is up 16% this year and 24% from its October 2022 low.

A recession does not describe the stock market, but the two are correlated, as they were post-Dot-Com bubble and during the Great Financial Crisis.

Recession fears caused many to forecast a dire near future for stocks. And indeed, 2022’s bear market looked uncomfortably like the first twelve months of the 2000-02 and 2007-09 bears.

However, 2023’s recovery has defied the pattern. Eighteen months in, the Dot-Com bear was still a year from its bottom, and the Great Recession bear had just reached its nadir. Here, the S&P 500 has climbed to within 7% of its high.

Analysts tend to fall in love with their predictions. Many continue to warn about a coming recession and naysay 2023’s resurgence – it’s unsustainable, just a handful of companies are driving returns, the Fed rate rise effect is lagging, etc.

A recession may indeed be around the corner. Yet, those that let that expectation drive portfolio decisions have watched a strong rally from the sidelines. When the recession does come, and one will eventually, an attractive stock market entry point may have already passed.

II. Recent Portfolio Changes

We made portfolio changes over the last month. There were a couple common and complementary goals –

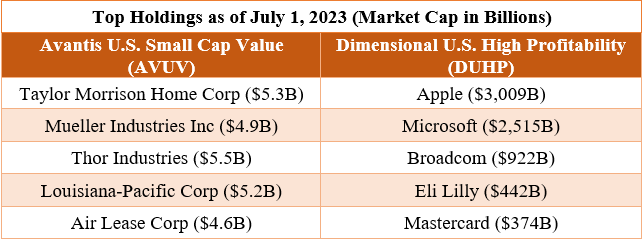

- Increase exposure to U.S. small cap value stocks

- Introduce a fund that focuses on highly profitable U.S. large cap stocks

Put simply, buying value stocks aims to buy average companies at low prices. Buying high profitability stocks aims to buy great companies at average prices.

We expect that the combination will improve our portfolio’s diversification benefits and long-term results.

U.S. Small Cap Value

In October, we discussed the addition of a U.S. small cap value fund.

As a refresher, small cap refers to the size of the company (cap = capitalization or total value of all shares). Value means buying companies with low prices relative to their fundamentals, e.g., profits.

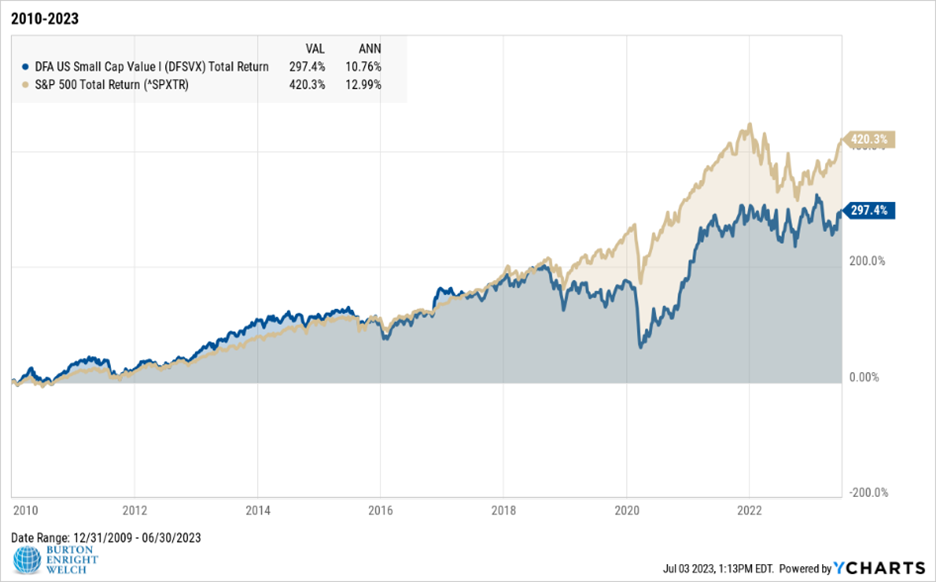

Small value is a relatively tiny corner of the market that has had outsized long-term returns. Since 1950, U.S. small cap value has an annualized 15.1% return versus 11.3% for the S&P 500.

More recently, small cap value had a stellar first decade of the century while the S&P 500 produced a negative return.

The relationship flipped the last dozen years and particularly the last five.

The addition of U.S. small cap value reflects our expectation that the asset class’s outperformance will recur long-term.

Still, higher returns are not a “free lunch.” Small cap value is a volatile part of the market. Smaller companies are more economically sensitive – they are generally more regional, less diversified, and more dependent on the health of the overall economy.

That volatility, in part, explains our addition of a fund focused on highly profitable U.S. companies.

U.S. High Profitability

Investing in value stocks has been a popular strategy among academics and evidence-based investors for decades. The profitability factor (similar to the popular quality factor) is more recent.

The profitability factor scours financial reports to identify companies with high and consistent profits, efficient operations, and low debt. Unlike small value, the resulting portfolio spotlights large, well-known firms.

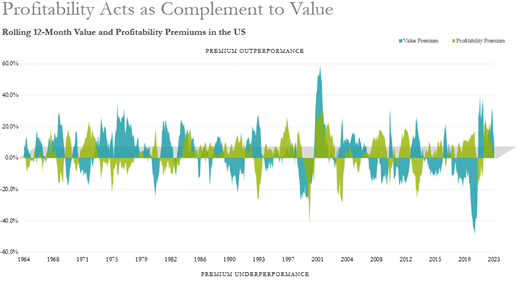

The next chart divides the stock market into two buckets based on profitability. It then looks at how the high profit bucket performed against the low profit bucket over different time periods.

We recognize that a strategy focused on highly profitable companies seems like stating the obvious – like why more money is better than less.

Why is there an opportunity? Shouldn’t profits attract investor demand, driving stock prices up and negating the benefit?

Like the value factor, no one is sure why the profitability factor consistently outperforms. A few theories include:

- Investors are drawn to speculative stocks (i.e., low profits today, will be massive in the future). Investing in profitable businesses is relatively boring. Slow-and-steady wins the race.

- During economic downturns, profitable companies are more resilient, so their drawdowns are shallower.

- Many investors overemphasize short-term news and drama. They underappreciate a persistent, unexciting long-term story.

While the profitability factor’s outperformance is compelling on its own, profitability’s story is strongest when paired with value.

The chart above illustrates when the value and profitability factors outperform. At times, they coincide. Occasionally, they both underperform like during the Dot-Com bubble. But mostly, they outperform at different times.

This is the essence of diversification, the lone way to increase expected returns with lower risk. One asset class’s excellence while the other lags reduces the depths of declines, provides a smoother ride, and improves long-term returns.

That smoother ride is particularly desirable when taking regular distributions (e.g., retirees). Higher returns with higher volatility may cause worse results due to the times investors must sell depressed investments to take distributions.

We have plenty more we can share on this topic. If you are curious, we’re happy to go in more depth and review the trades in your portfolio.

We hope everyone is having a fun and safe summer!

Get the BEW Newsletter Direct to Your Inbox

Stay informed with timely perspectives and market insights from the BEW Invest team.