Similar to markets, the topics we expect to cover in a quarterly commentary can shift quickly.

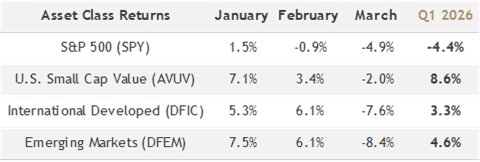

After January, we might have focused on the continued strength of international stocks. After February, the conversation may have turned to a resurgence in small cap stocks alongside a lagging S&P 500.

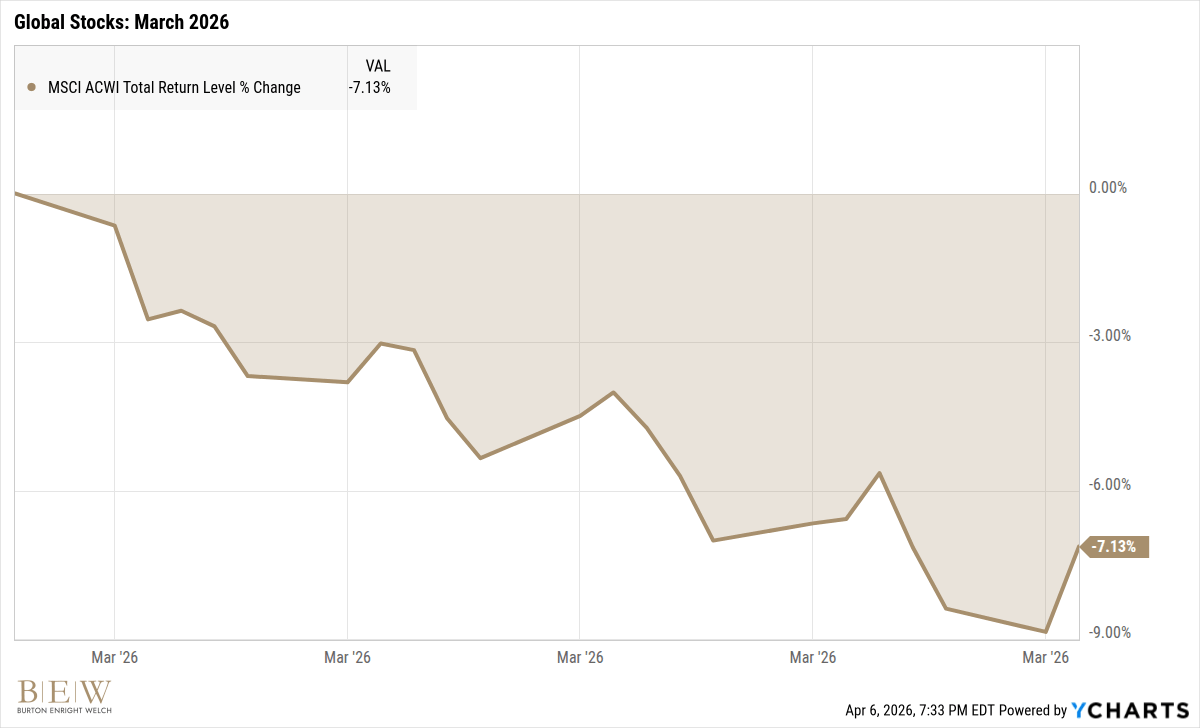

But by the end of March, those themes had largely faded into the background. Conflict in Iran, rising oil prices, and the resulting market pullback became the story of the quarter.

Portfolios with meaningful gains through the first two months finished the quarter with little to show for it.

Yet, without those earlier gains, the story of Q1 would look much worse.

Imagine if March had been January. With the page turned, seeing a relentless slide to start the year would have generated more anxiety. Last year’s strong returns were already celebrated and memorialized. It would have felt like 2026 was off to an ominous start.

Instead, with strong January and February returns in our pockets, March’s volatility was easier to swallow. Where you start the clock often determines how you feel about the result. That seemingly arbitrary detail can end up shaping the entire story.

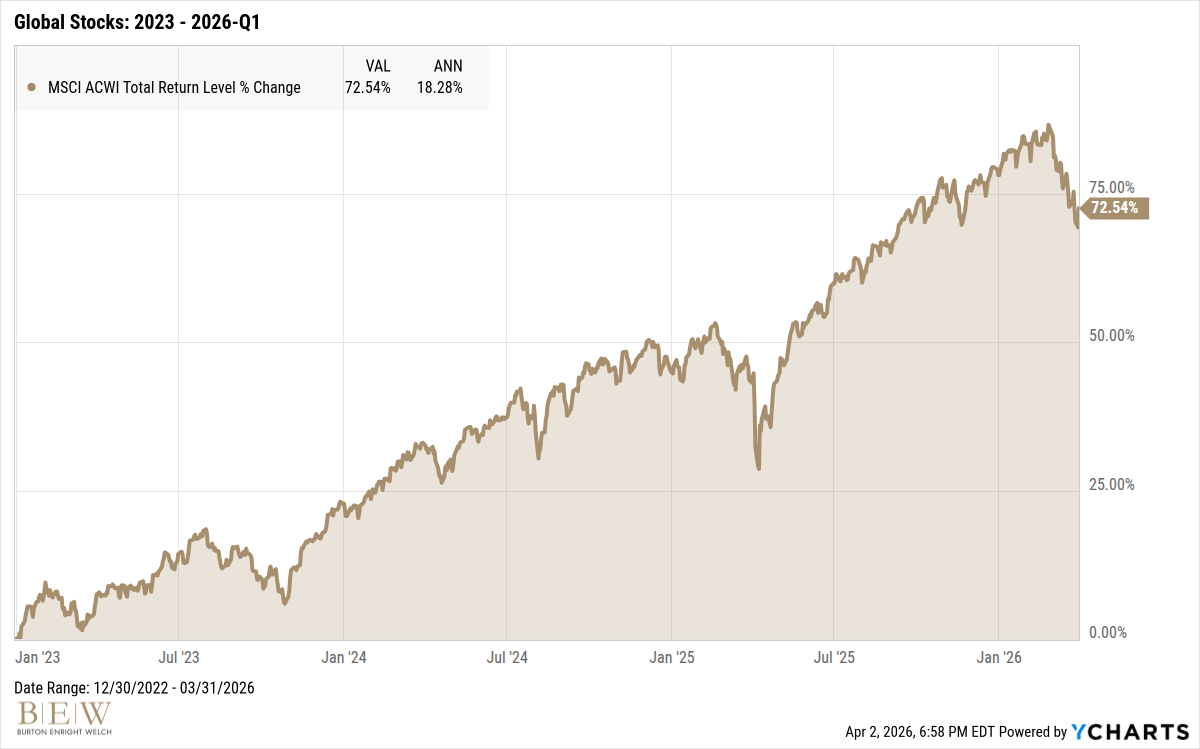

Start the clock in 2023 and it looks like a one-way trip up-and-to-the-right with a few pullbacks.

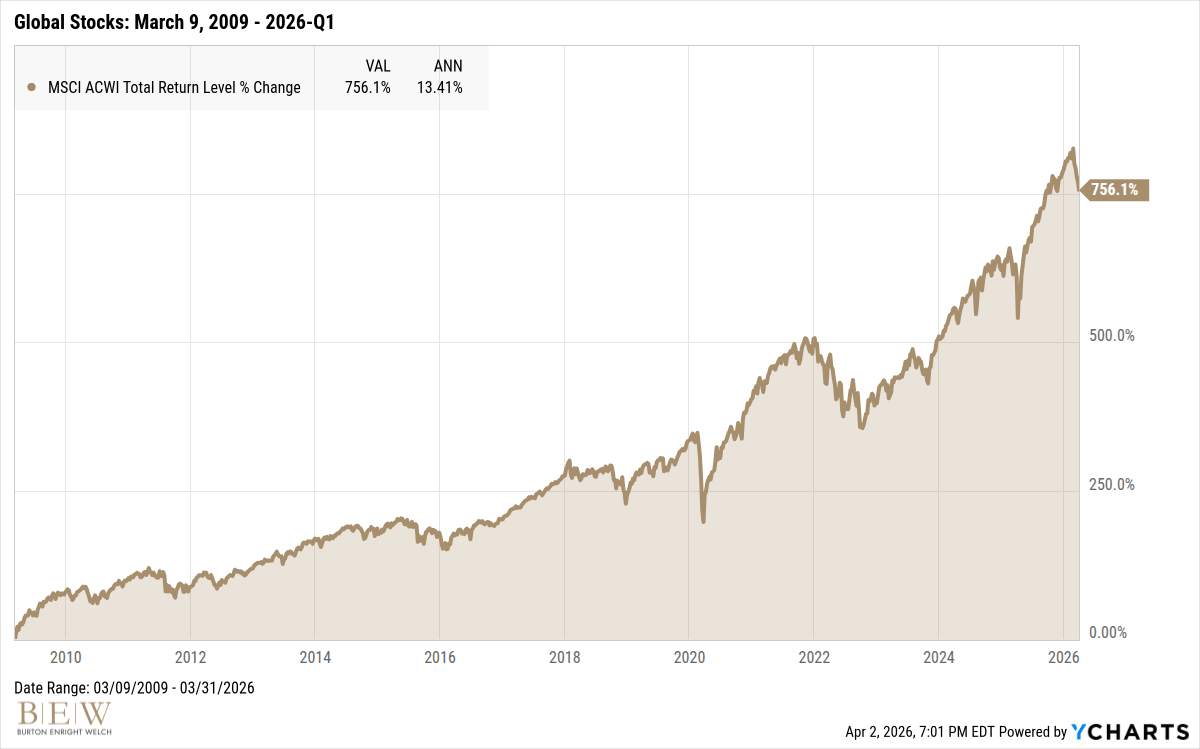

Even more to the point, start the clock on March 9, 2009…

… and events like Covid, 2022’s inflation, and Liberation Day look like minor interruptions.

Geopolitics Matter, But in Context

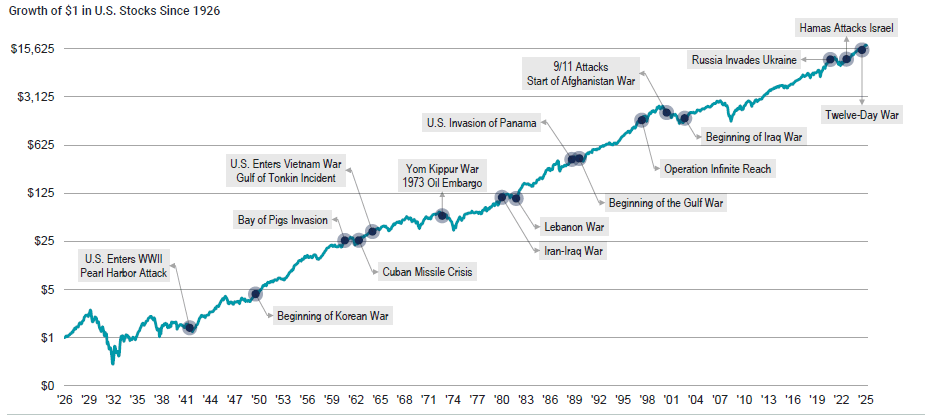

Long-term perspective is a powerful tool. It can shrink meaningful short-term concerns into what looks like a small blip within a much larger trend of growth.

But this framing can also feel a bit too convenient.

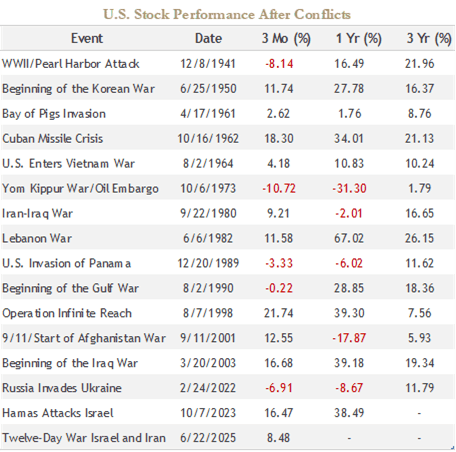

Geopolitics matter. Wars matter.

While the long-term is far more important for investors with a lifetime of goals and spending needs, that does not mean we should ignore current events. It’s still worth asking what the past tells us.

With geopolitics and wars, there is a long history of markets behaving in ways that are difficult to predict.

The only consistent pattern is that markets have been higher three years later. Markets have declined during some conflicts, risen during others, and often recovered faster than expected. Events that felt consequential at the time didn’t translate into long-term market losses.

It’s not that geopolitics don’t matter. Rather, they are one input of many. Interest rates, inflation, earnings, and investor expectations are all moving at the same time.

Isolating the impact of any single event, no matter how significant, is treacherous. A prognosticator may be right about an event’s impact and overriding factors may still cause the market prediction to be far off.

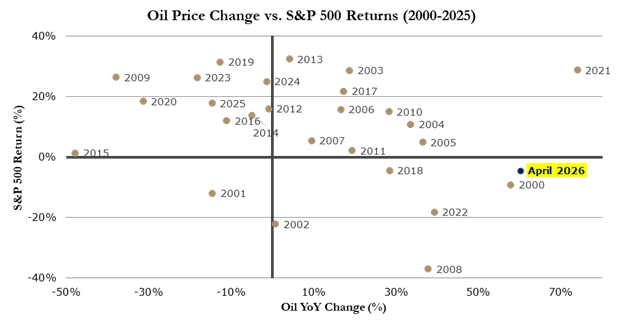

Take recent concerns around rising oil prices. Higher oil prices are viewed as a market headwind. And intuitively, this makes sense. But, the relationship between oil and stock market returns has been inconsistent.

Oil prices may indeed be a net negative for markets – raising inflation, reducing consumer spending, and pressuring corporate margins through higher input costs.

But oil is only one of many forces moving markets. Today, artificial intelligence is a major driver of both current profits and future expectations. Over the long run, the war in Iran may register as a brief disruption compared with A.I.’s influence on the global economy.

And while higher oil prices can be a challenge, the economy is remarkably adaptable. Businesses adjust, supply chains shift, and consumers change behavior. What begins as a headwind often becomes something the system absorbs and learns to work through.

This is what makes investing through periods of uncertainty so challenging. The instinct is to assume that big events should produce clear, zero-sum outcomes. But the relationship is rarely that direct. Businesses have a long track record of adapting, adjusting, and moving forward despite challenges.

In many cases, the biggest risk isn’t the event itself – it’s how investors respond to it.

Trust the Process, Especially in Turmoil

In other fields, success often comes down to a repeatable process, especially when pressure is highest.

In The Power of Habit, Charles Duhigg tells the story of Tony Dungy’s coaching career. Early on, Dungy was often passed over for head coaching roles because his philosophy was perceived as too simple.

But that simplicity was intentional.

Dungy wanted his players to rely on a repeatable system so they didn’t have to make split-second decisions under pressure. The problem arose when players abandoned that system in critical moments.

“We would practice, and everything would come together and then we’d get to a big game, and it was like the training disappeared,” Dungy explained. “Afterward, my players would say, ‘Well it was a critical play and I went back to what I knew,’ or ‘I felt like I had to step it up.’ What they were really saying was they trusted our system most of the time, but when everything was on the line, that belief broke down.”

What ultimately changed was not the system, it was players’ commitment to it (Dungy won a Super Bowl with the Indianapolis Colts). Success came when they trusted the process, not just when it felt easy or intuitive.

Investing is no different.

Uncertainty is not unusual, it’s constant. Periods like March increase its visibility. Headlines become more frequent, market moves feel more meaningful, and the urge to “do something” increases. But these are often the moments when sticking to a sound process matters most.

A well-constructed portfolio is built with this in mind. Diversification, long-term thinking, and rebalancing are not designed for calm environments. They are designed for periods like this.

That doesn’t mean ignoring markets or tuning out information entirely. It means recognizing that reacting to short-term developments, especially those tied to unpredictable events, is unlikely to lead to better outcomes.

Over time, the most reliable driver of results has not been the ability to anticipate events, but the ability to stay invested through them.

Get the BEW Newsletter Direct to Your Inbox

Stay informed with timely perspectives and market insights from the BEW Invest team.