I. The Case for Diversification Remains Strong

Remarkably, the 2020s are half over! The 21st century is at the quarter mark. We are closer to 2100 than to WWII.

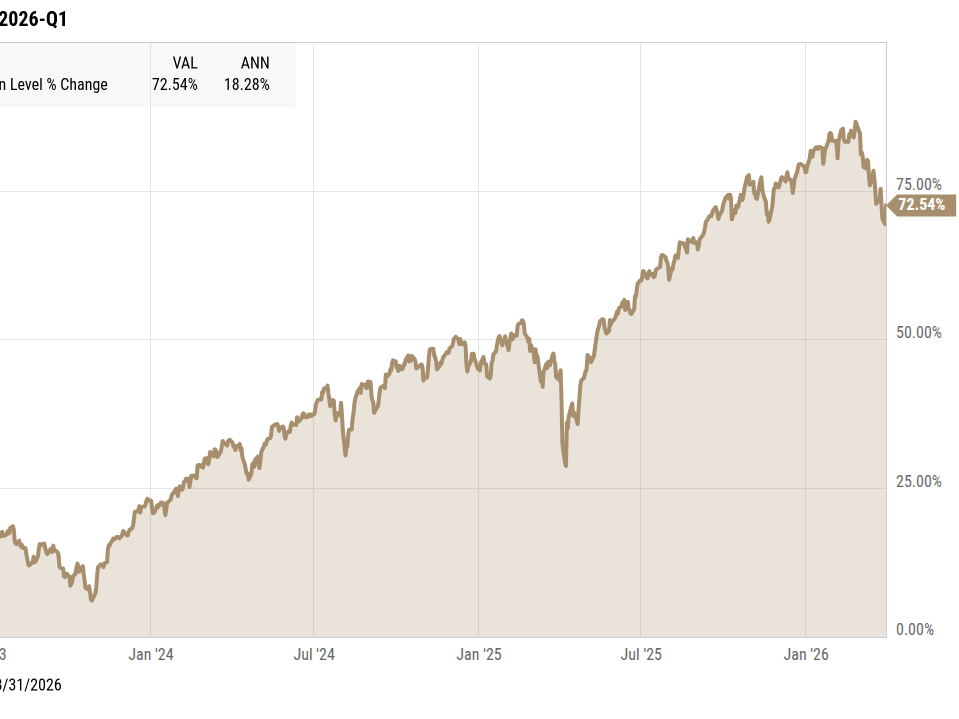

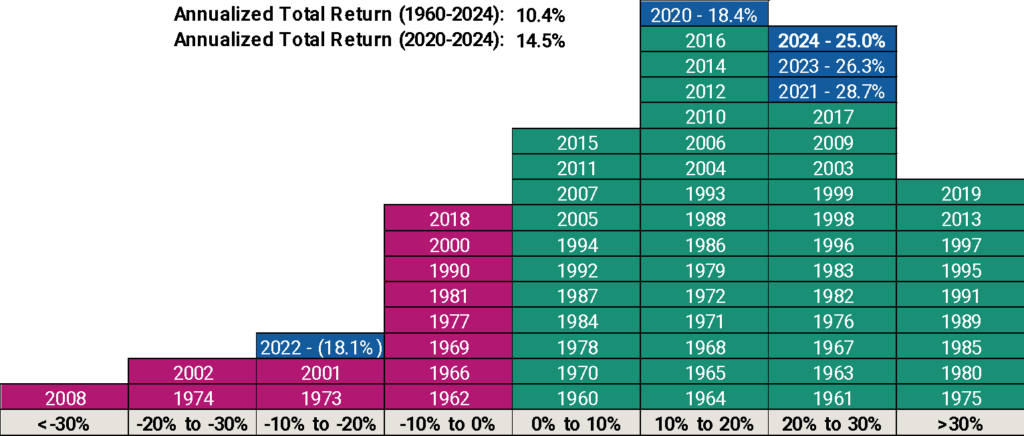

Fittingly for a dramatic decade, every year has featured a big move for the S&P 500 – either far above or far below its ~10% long-term average (see blue boxes above).

Big moves are not unusual. Above, notice how uncommon annual returns are 0-10%. Stocks produce long-term averages through a two-step-forward-one-step-back rhythm. This decade, the S&P 500 has delivered 14.5% per year, nearly 100% in total returns.

The S&P 500 represents about 5% of publicly listed companies and about half of the global stock market’s value. Yet, in reputation it punches far above its weight.

It is common to hear versions of “just invest in the S&P 500 and call it a day.” And, with hindsight, that would have worked well for much of the last fifteen years.

Our portfolios have large positions in S&P 500 stocks. Their top three holdings are NVIDIA, Apple, and Microsoft. We hope that the S&P 500 will continue its streak.

Our portfolios also own other asset classes that, despite solid-to-good results, underwhelm relative to the S&P. We must prepare for the possibility of prolonged poor performance by the S&P. We don’t have to look back far for that lesson.

Beyond just defense, diversification also can improve results, even if it doesn’t appear to work often.

Let’s review our non-S&P asset classes. Despite recent years, the case for diversification remains strong.

1. International Stocks

“Diversification protects against the unknown, but it feels like a drag when the known is doing just fine.”

– David Swensen, former Yale endowment manager

The current sentiment on international stocks is brutal.

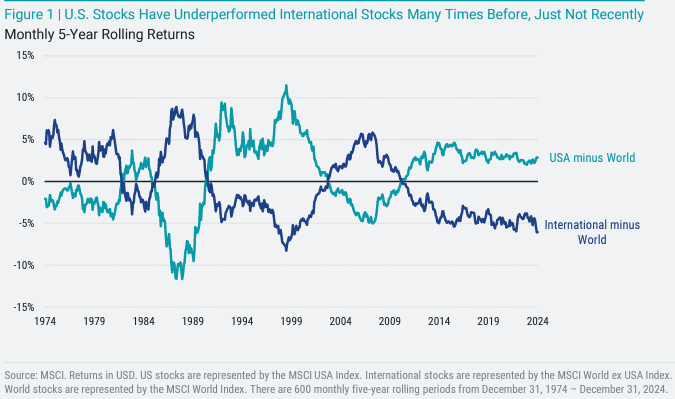

Despite a long track record, higher dividends, superior valuations, and stronger economic growth (Asia), returns have trailed U.S. stocks for most of the last decade-plus.

On the one hand, market history is brimming with examples of strategies, geographies, and factors going in and out of favor. Nothing works forever.

On the other, the world has never seen profit-printing behemoths like today’s U.S. corporate giants. The U.S. has the world’s most dynamic capital markets and drives the lion share of global innovation.

Our portfolios will continue to capture the value created by large U.S. companies. Artificial Intelligence is the latest example of American industry unlocking giant new opportunities for long-term growth.

Set aside the case for international stocks on their own merits. The diversification case for international stocks is robust. Here are evergreen reasons to own international:

- Extreme underperformance can strike single markets, even economic powers (see Japan post-1990)

- Hedge against a weakening U.S. dollar

- Domestic political risk

- Sector diversification

- Economic diversification – most of our lives rely on the health of the U.S. economy

- There are world class companies overseas that do not have a U.S. equivalent, e.g. LVMH (France), Nestlé (Switzerland), and Taiwan Semiconductor.

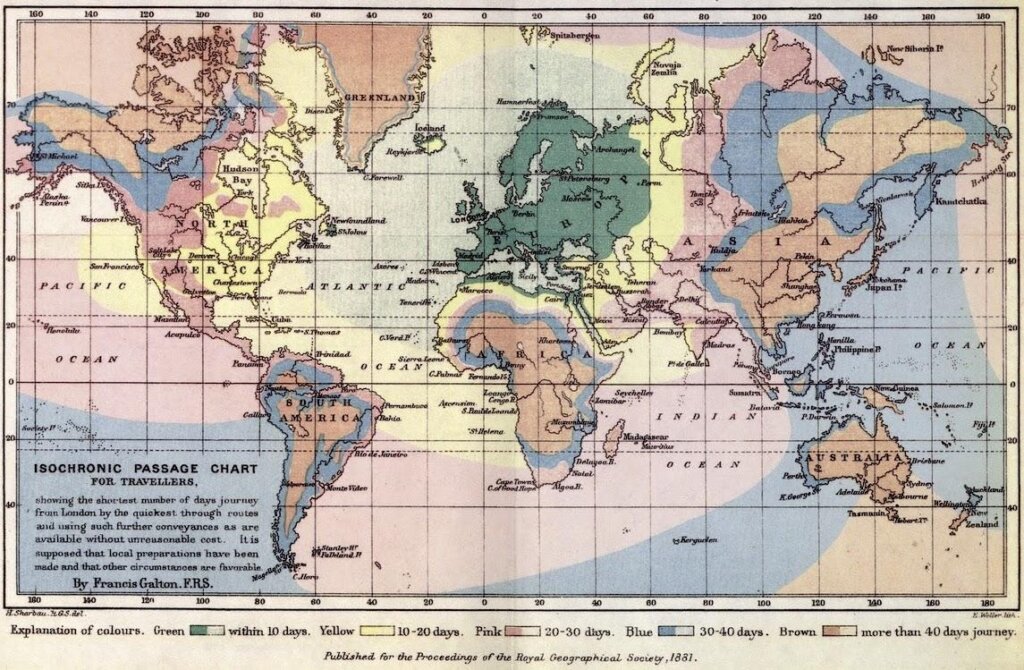

Next is an 1881 map of the world. Colors signal how many days it took to travel from London. Brown shows how much of the world was a 40+ day journey away.

Today, with a few clicks, money can travel the world instantly, purchasing shares of global companies. It is no easier or cheaper to own U.S. stocks.

A preference for U.S. stocks is understandable. But excluding international stocks is risky.

Diversification helps avoid extremes. It ensures never being fully invested in the best performer and never being fully invested in the worst.

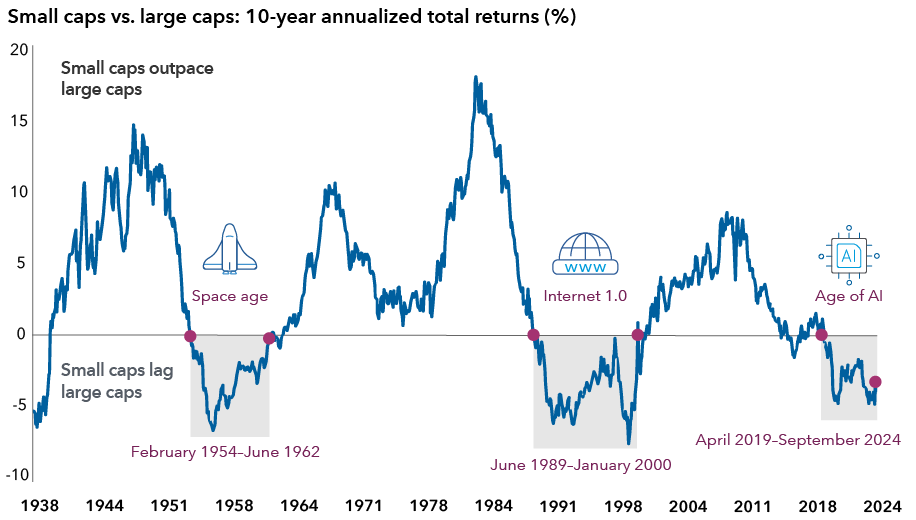

2. Small Cap Stocks

“The job of an investor is not to make the most money possible. It’s to avoid the mistakes that will take you out of the game. Diversification is your insurance policy.” -Jason Zweig, Wall Street Journal

Like international stocks, small cap stocks have yo-yoed versus the S&P 500. Also similarly, they are amid a long period of underperformance.

Last year’s 11.5% return for the Russell 2000 index of small cap stocks fell short of the S&P 500 for the fourth year in a row and seventh of the last eight.

While the relationship is cyclical, over most long-time periods, small caps have outperformed large caps, including 70% of three-year periods this century.

Higher long-term returns for small caps aligns with theory. Investors require greater compensation for the added risk of more volatile, economically sensitive businesses.

Small caps may have underperformed recently in part due to the technology cycle. Major tech shifts – like the Space Race, internet boom, and smartphone era – generate benefits that take time to accrue to smaller companies.

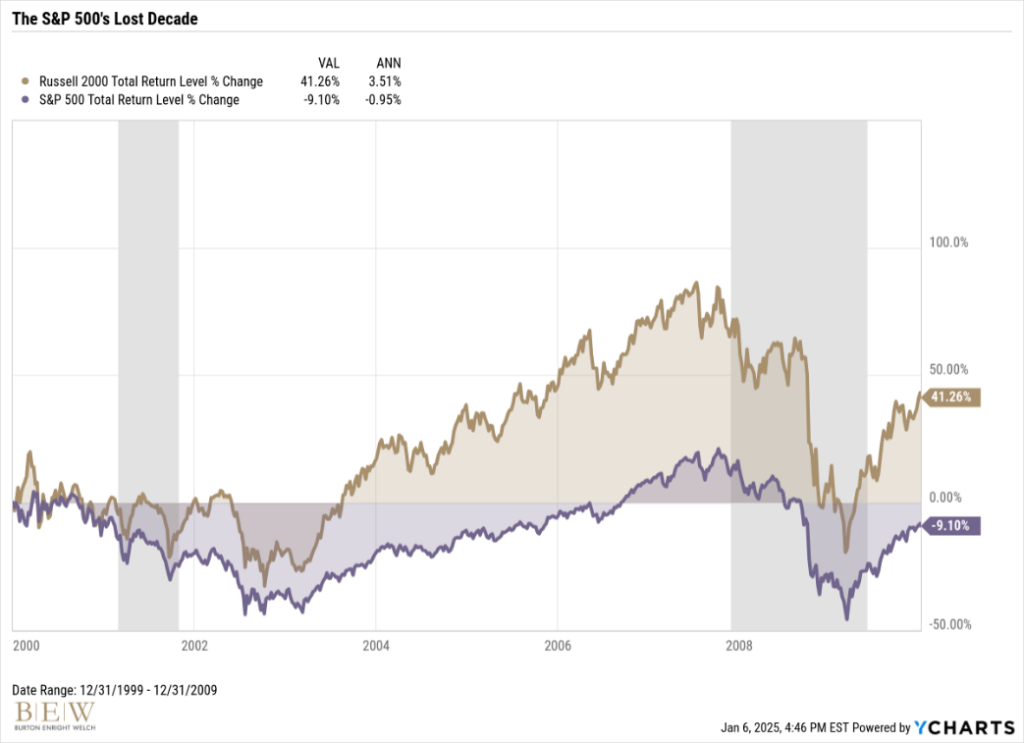

Small caps also diversify against large cap risks. The 2000s weren’t a lost decade for the U.S. stock market. They were a lost decade for the S&P 500. Small cap stocks far outpaced the S&P 500 despite two recessions.

3. Bonds

“Diversification guarantees you’ll never hit a grand slam – but it also keeps you from striking out.”

– John Bogle, founder of Vanguard

We expect bonds to underperform the S&P 500.

Stocks compensate for their unpredictability by delivering higher long-term returns.

Bonds are contracts. Their promises make returns predictable, but limit upside.

Despite more modest expected results, we own bonds for capital preservation, income, and diversification against stock risk. For our clients in or near retirement, we gladly trade better long-term expected returns for predictability.

Bonds had a rough 2024 – the broad bond index returned 1.3%. This is shortly on the heels of 2021 and 2022, back-to-back negative years due to steep rate rises by the Fed.

On one level, bonds have not worked as intended. There is no sugarcoating negative returns.

On another level, this is diversification – when one asset class performs poorly, another picks up the slack.

In the past, when stocks struggled, bonds often kept portfolios afloat.

If we divide the quarter century into halves, in the first half bonds outperformed stocks by 5% per year, or ~100%!

The latter half, stocks rewarded investors. Though meager, the second half’s bond returns still beat the S&P 500 returns in the first half.

Of course, if we knew that current trends would continue, we’d shun bonds.

Diversification is a concession to the unknowability of the future. There will be a period when bonds do the heavy lifting again.

And as that period may last a decade or longer, plenty of investors – particularly those who take regular distributions – cannot afford to own just stocks.

4. Diversification Doesn’t Have to Work Often to Work

“The greatest mistake investors make is to believe that what happened in the past will inevitably happen in the future. Diversification ensures that you don’t have to get everything right to do well enough.”

– Peter Bernstein, economist and author

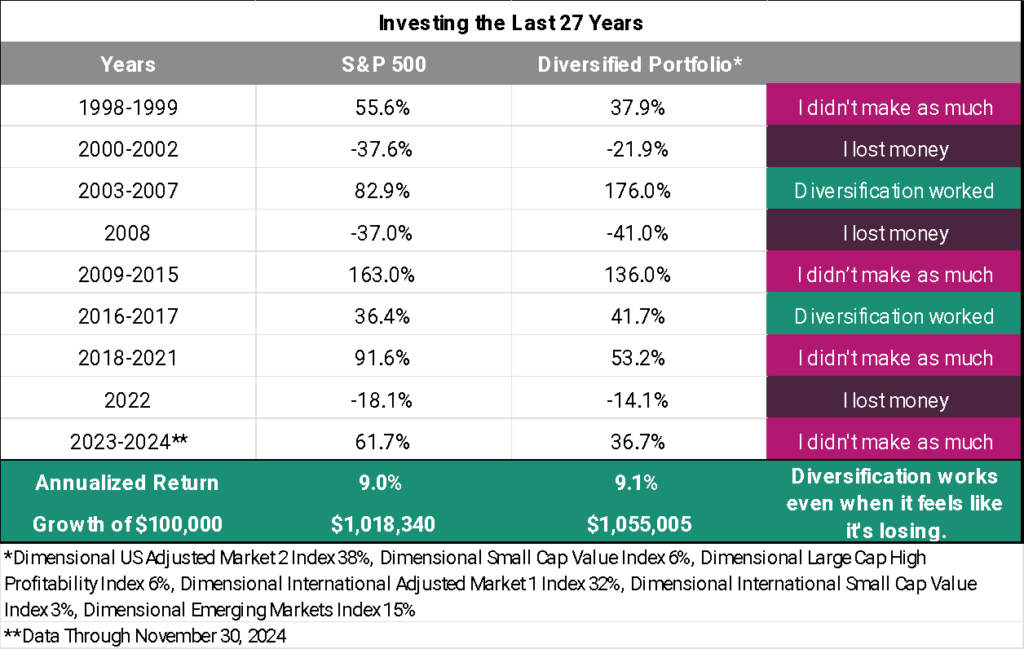

The magic of diversification isn’t that you don’t lose, or even that you don’t occasionally lose big. It’s the improved compounding of returns a smoother ride provides – when the lows aren’t as low, even if the highs aren’t as high.

The next chart shows the S&P 500 versus a 50% U.S. stocks and 50% international stocks Diversified Portfolio, which also includes small cap and emerging market stocks.

From 1998 to 2024, despite a slow start, only two periods of positive outperformance, and long periods of international and small cap underperformance, the Diversified Portfolio outpaced the S&P 500.

Diversification doesn’t have to work often to work.

5. Diversification Balances Risk and Return

“History is never a straight line; it’s a long and winding road, often marked by unexpected turns. Diversification is how we prepare for the bends we can’t see.”

– ChatGPT-generated quote

Perhaps, our case for diversification over relies on lessons from the 2000s. The S&P 500 has transformed since the turn of the century. Amazon, NVIDIA, Google, Meta, and Tesla either didn’t exist or were not in the index then.

It’s also possible that the S&P 500’s meteoric rise is in large part due to its lost decade. Markets are cyclical – overperformance begets underperformance and vice versa.

Many past dominant trends seemed like they would last forever and eventually hit a wall, e.g., the Nifty Fifty of the 1960s and 1970s, Japanese stocks in the 1980s, dot-com stocks in the 1990s, and energy stocks in the 2000s.

It’s naïve to assume that history will repeat, that investing is just about cycles.

It’s also naïve to assume that diversification is obsolete.

Our goal is to deliver a reliable return to enable clients to meet their needs now and in the future. Diversification remains the most effective strategy to safeguard against uncertainty while positioning for long-term success.

II. Social Security for Public Sector Employees

Last week, President Biden signed the Social Security Fairness Act (SSFA). The SSFA enables or increases Social Security benefits for millions of public sector workers and their spouses.

The legislation, which passed with broad bipartisan support, eliminates the 40+ year old Windfall Elimination Provision (WEP) and Government Pension Offset (GPO).

The WEP impacted police officers, firefighters, teachers, etc., who also have worked 10+ years in the private sector. It often reduced or eliminated their Social Security benefits, despite having paid into the system.

Similarly, the GPO reduced spousal Social Security benefits for spouses and surviving spouses who earned a public pension.

Estimates are that the SSFA will increase benefits for 2-3 million retirees, including some who were previously ineligible for Social Security.

The SSFA will be retroactive to 2024, meaning eligible beneficiaries will receive a lump sum payment for the benefits withheld due to the WEP and GPO in the past year.

Updated benefits should come automatically, though it may take many months for the Social Security Administration (SSA) to operationalize the new rules. Here is a website for SSA updates on implementation.

While the SSFA is a major victory for the affected retirees, it comes at a significant cost – approximately $200 billion over the next decade. With the Social Security trust fund projected to be depleted by the mid-2030s, this change will increase the urgency for Congress to address the program’s long-term solvency.

Please contact your advisor if you have any questions about your eligibility.

Get the BEW Newsletter Direct to Your Inbox

Stay informed with timely perspectives and market insights from the BEW Invest team.